Futures Market: LME copper was closed overnight. The most-traded SHFE copper 2502 contract opened at 74,180 yuan/mt overnight, initially hitting a high of 74,210 yuan/mt before fluctuating downward to an intraday low of 74,070 yuan/mt. It then fluctuated upward and consolidated sideways at the end, finally closing at 74,160 yuan/mt, up 0.14%. Trading volume reached 6,000 lots, and open interest stood at 139,000 lots.

【SMM Copper Morning Meeting Notes】News: (1) The Bank of Korea stated that due to increased political uncertainty and other downside risks, it plans to further lower the benchmark interest rate in 2025. The Bank of Korea also pledged to implement market stabilization measures at an appropriate time if necessary. (2) The National Housing and Urban-Rural Development Work Conference was held in Beijing. The meeting outlined five key tasks for national housing and urban development in 2025, including persistently promoting the stabilization and recovery of the real estate market, fostering a new model for real estate development, vigorously implementing urban renewal, upgrading "China Construction," and building safe, comfortable, green, and smart housing. Among these, persistently promoting the stabilization and recovery of the real estate market was prioritized.

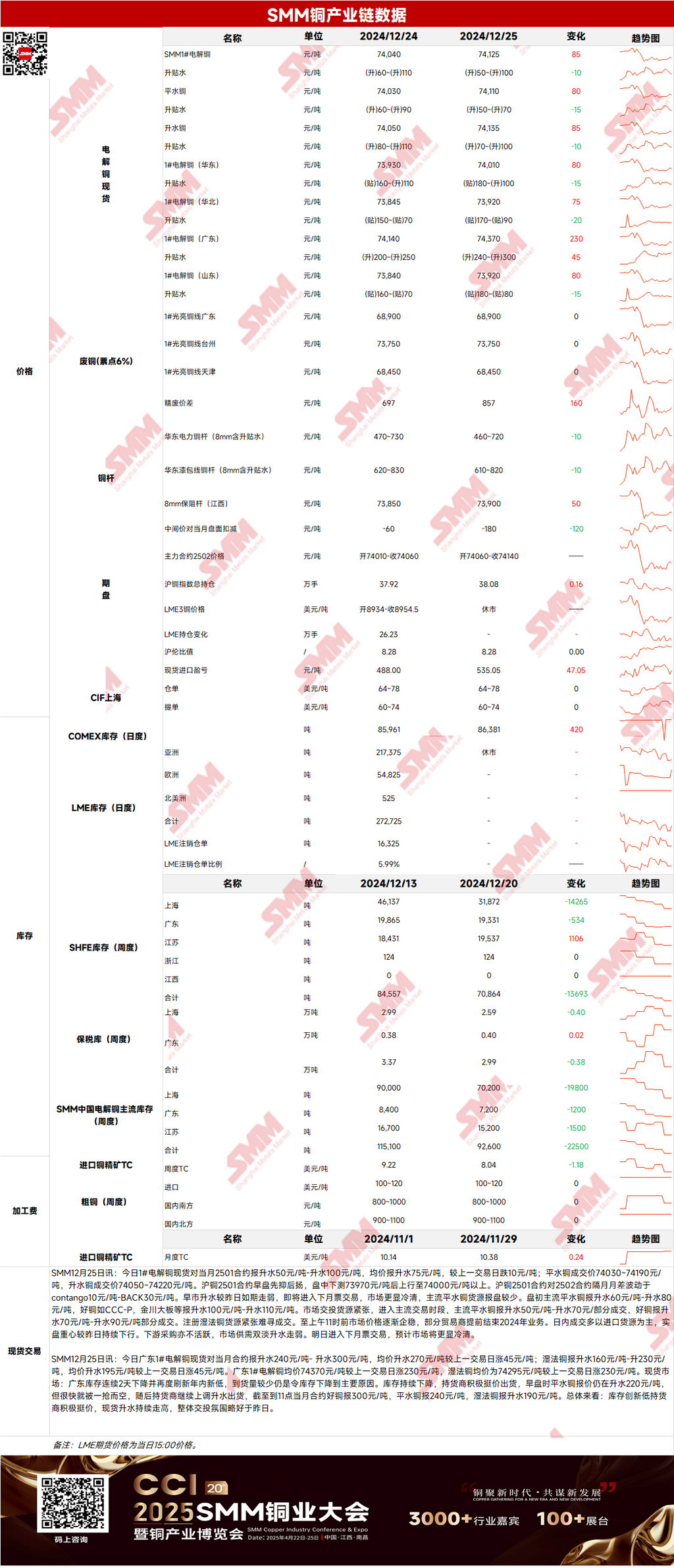

Spot Market: (1) Shanghai: On December 25, #1 copper cathode spot premiums against the front-month 2501 contract were quoted at 50-100 yuan/mt, with an average of 75 yuan/mt, down 10 yuan/mt MoM. Transactions yesterday were mainly for imported cargoes, with the trading center continuing to decline compared to the previous day. Downstream purchasing was also inactive, and both supply and demand in the market were weak, leading to lower premiums. As trading shifted to cargoes with invoices dated next month, the market is expected to become even quieter today.

(2) Guangdong: On December 25, #1 copper cathode spot premiums against the front-month contract were quoted at 240-300 yuan/mt, with an average of 270 yuan/mt, up 45 yuan/mt MoM. Overall, inventory hit a record low, and suppliers stood firm on quotes, pushing spot premiums higher. The overall trading atmosphere was slightly better than yesterday.

(3) Imported Copper: On December 25, warehouse warrant prices were $64-78/mt, QP January, with the average price flat MoM; B/L prices were $60-74/mt, QP January, with the average price flat MoM; EQ copper (CIF B/L) was quoted at $14-28/mt, QP January, with the average price flat MoM. Quotes referenced cargoes arriving in late December and early January. Due to the Christmas holiday closure of LME copper and the already limited supply, the US dollar-denominated copper market was relatively quiet today.

(4) Secondary Copper: On December 25, secondary copper raw material prices remained unchanged MoM, with Guangdong bare bright copper prices at 68,800-69,000 yuan/mt, unchanged from the previous trading day. The price difference between primary metal and scrap was 857 yuan/mt, up 160 yuan/mt MoM. The price spread between primary and secondary copper rods was 770 yuan/mt. According to the SMM survey, the price spread between primary and secondary copper rods slightly widened today, but sales of secondary copper rods were average. Many sales managers at secondary copper rod enterprises indicated that the consistently low price spread between primary and secondary rods led end-user wire and cable enterprises to maintain just-in-time procurement. Additionally, some end-users stated that they would stop placing new orders after the New Year holiday. Current raw material inventories are sufficient to meet production needs for orders on hand, resulting in lackluster trading for secondary copper rods today.

(5) Inventory: On December 25, LME copper cathode inventory increased by 0 mt to 272,725 mt; SHFE warehouse warrant inventory decreased by 856 mt to 14,659 mt.

Prices: Macro side, the PBOC conducted 192.3 billion yuan of 7-day reverse repo operations. Macro analyst Qing Wang stated that although the peak of local government bond issuance has passed, the PBOC may cut the RRR by 0.25-0.5 percentage points by year-end to support banks in increasing credit issuance, continue supporting government bond issuance, and sustain growth-stabilizing signals. Meanwhile, the policy signals released by the recent domestic fiscal work conference have boosted market sentiment, stabilizing copper prices. However, the US dollar index remained at high levels, which will exert some pressure on copper prices. Overall, copper prices lack further upward momentum. Fundamentals side, supply side, domestic copper cathode circulation was limited, with most transactions involving imported cargoes during the day. Demand side, downstream purchasing sentiment was average, with overall purchasing as needed. As trading shifted to cargoes with invoices dated next month, the market is expected to become even quieter. Copper prices are expected to fluctuate rangebound at current levels today.

》Click to View the SMM Metal Database

【The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided herein is for reference only and does not constitute direct investment research advice. Clients should make prudent decisions and not substitute this for independent judgment. Any decisions made by clients are unrelated to SMM.】